‘Underwater’ Homeowners Rise to 28 Percent: Zillow

By - May 9, 2011 4:19 PM ET

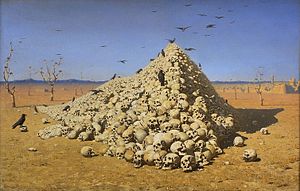

Rows of houses stand in Las Vegas in an aerial photo taken on Sept. 22, 2009. Homeowners with negative equity increased to 28 percent nationwide from 22 percent a year earlier, according to Zillow Inc. Photographer: Jacob Kepler/Bloomberg

Homeowners with negative equity increased from 22 percent a year earlier as home prices slumped 8.2 percent over the past 12 months, the Seattle-based company said. About 27 percent of homes with mortgages were “underwater” in the fourth quarter, according to Zillow, which runs a website with property-value estimates and real-estate listings.

Home prices fell 3 percent in the first quarter and will drop as much as 9 percent this year as foreclosures spread and unemployment remains high, Zillow Chief Economist Stan Humphries said. Prices won’t find a floor until 2012, he said.

“We get tired of telling such a grim story, but unfortunately this is the story that needs to be told,” Humphries said in a telephone interview. “Demand is still quite anemic due to unemployment and the fact that home values are still falling. And that tends to make people more cautious about buying.”

The U.S. unemployment rate rose to 9 percent in April, up from 8.8 percent in March, the Department of Labor reported May 6. Home prices have fallen almost 30 percent from their June 2006 peak, wiping out more than $10 trillion in equity, including $667.5 billion in the first quarter, Humphries said.

Dropping Home Values

Other analysts also expect homes to continue losing value this year. Oliver Chang of Morgan Stanley expects prices to fall as much as 11 percent, according to an April 25 report. Prices may fall “another 5 or 10 percent,” Robert Shiller, an economics professor at Yale University, told Fox Business on April 26. Home prices were 33 percent below the July 2006 peak in February, according to the S&P/Case-Shiller Composite 20-City Home Price Index, co-created by Shiller.Prices will continue falling as more houses are lost to foreclosure, flooding the market with distressed properties, Humphries said.

Foreclosures fell to the lowest level in three years in the first quarter as lenders worked through a backlog of flawed paperwork, according to RealtyTrac Inc., an Irvine, California- based real estate information service. Foreclosure filings are likely to jump 20 percent this year, reaching a peak for the housing crisis, RealtyTrac predicted in January.

The number of homes with negative equity rose to 16.2 million in the first quarter from 13.1 million a year earlier, Zillow said.

Las Vegas Highest

In Las Vegas, 85 percent of homes with mortgages were underwater, the most of any city tracked by Zillow. Other metropolitan areas in the top five were Reno, Nevada, at 73 percent; Phoenix at 68 percent; and Modesto, California, and Tampa, Florida, both at 60 percent. Zillow has tracked negative equity since the first quarter of 2009, when more than 22 percent of homes were underwater.

Property values rose in only three of the 132 regions tracked by Zillow: Fort Myers, Florida, where they gained 2.4 percent; Champaign-Urbana, Illinois, up 0.8 percent; and Honolulu, up 0.3 percent. Fort Myers prices increased after falling more than 60 percent from their 2006 peak because they “over-corrected,” Humphries said.

The first quarter’s U.S. home price decline was the steepest since the fourth quarter of 2008, when prices fell 3.9 percent, according to Zillow data. Values dropped almost 13 percent over the course of that year.

“It’s not going to be as bad as 2008,” Humphries said. “But it’s going to be worse than we thought it was going to be.”

‘Stealing Demand’

Prices were propped up in 2009 and early 2010 by federal stimulus programs, such as tax credits worth up to $8,000 for first-time homebuyers, Humphries said. That program “was stealing demand from the future,” weakening shoppers’ appetites now even as housing affordability is at its three-decade high, he said.“In the past, people felt more bullish in a post-recession recovery,” he said. “They’d go out and spend more on homes and that would ignite hiring in construction and the mortgage industry. And they’d start to get the flywheel moving more quickly. Unfortunately, now, that flywheel is broken.”

No comments:

Post a Comment